Aussie shares have tumbled and oil is surging, after US President Donald Trump threatened to send Iran "back to the Stone Ages" while declaring his military campaign nearly complete.

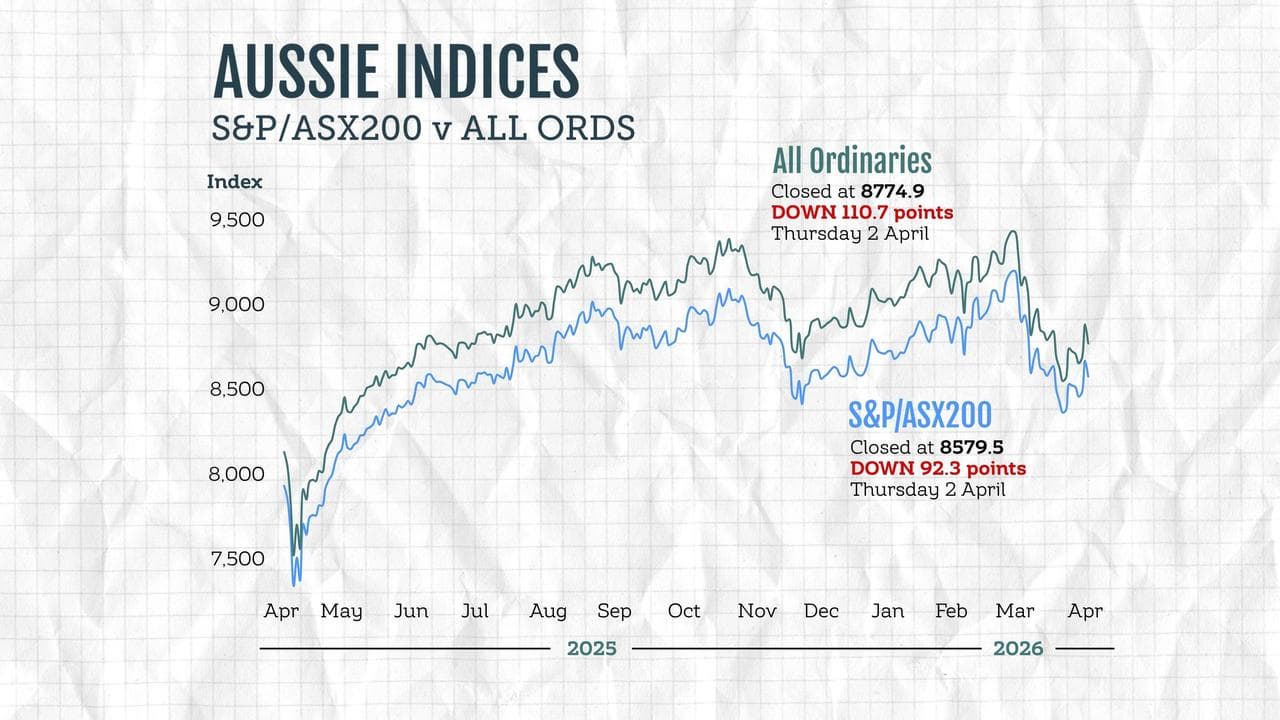

The S&P/ASX200 reversed early gains to end 92.3 points lower on Friday, down 1.06 per cent, to 8,579.5, as the broader All Ordinaries lost 110.7 points, or 1.25 per cent, to 8,774.9.

The retreat came after Mr Trump used a prime-time address to announce the Iran conflict would end soon, but not before the US ramped up its attacks, including on energy infrastructure if no deal was reached.

"We are going to hit them extremely hard over the next two to three weeks,” Mr Trump said.

“We’re going to bring them back to the Stone Ages.”

He offered no plan to reopen the blockaded Strait of Hormuz, instead suggesting nations depending on oil shipped through it to buy US crude or "take" the strait themselves.

"Go to the strait and just take it, protect it, use it for yourselves," Mr Trump said.

"The hard part is done, so it should be easy.”

Oil prices, which had eased to around $US100 a barrel on hopes the campaign would be winding down, soared after the speech above $US107 by the ASX close.

Resurgent crude prices put an end to the week's equities rally, which had been mostly driven by misplaced Wall Street optimism, Moomoo market strategist Michael McCarthy said.

"The facts did not change,” Mr McCarthy told AAP.

"If anything, they deteriorated slowly, as the (Iran-backed) Houthis threatened to block off the other port of access for Persian Gulf oil producers.”

ASX-listed mining stocks sold off as risk sentiment weighed on the global growth outlook and commodity demand.

Gold stocks were under particular pressure as the precious metal slumped against a rising greenback to $US4,647 ($A6,757) an ounce.

Mega miners BHP, Rio Tinto and Fortescue also tumbled between 2.5 and four per cent.

The heavyweight financials sector, often viewed as a bellwether for the bourse, was surprisingly robust, fading less than 0.2 per cent as CommBank and ANZ offered some resistance against broader weakness.

Consumer discretionary stocks fell more than one per cent, after Kathmandu owner KMD Brands' share price tanked by more than half as it emerged from a trading halt on completing a leg of a key capital raise.

The traditionally defensive consumer staples sector jumped 1.3 per cent as investors looked for safety beyond the barrage of grim headlines.

Looking ahead, Oxford Economics’ expect the conflict to last roughly two months, with Strait of Hormuz traffic to rise to around 50 per cent capacity in May before gradually returning to normal by the end of 2026.

But with opportunities for de-escalation were narrowing, an extended conflict could spark a sharp recession for Australia, economist Harry McAuley said.

“Transport, manufacturing and mining are particularly vulnerable,” Mr McAuley wrote in a research brief.

If the war dragged on beyond May, Australian gross domestic product would likely grind to 1.4 per cent in 2026 before recovering to just 2.1 per cent in 2027, as $US150 a barrel oil prices pushed global inflation to 7.7 per cent, he wrote.

“Agriculture is similarly exposed and faces medium-term trade-offs between fertilising with more expensive, scarcer resources or lower yields,” Mr McAuley said.

The Australian dollar is buying 68.68 US cents, down from 69.05 on Wednesday at 5pm, the Aussie fading as risk sentiment soured.

ON THE ASX:

* The S&P/ASX200 fell 92.3 points, or 1.06 per cent, to 8,579.5.

* The broader All Ordinaries lost 110.7 points, or 1.25 per cent, to 8,774.9.

One Australian dollar trades for:

* 68.68 US cents, from 69.05 US cents at 5pm AEDT on Wednesday.

* 109.46 Japanese yen, from 109.50 Japanese yen.

* 59.58 euro cents, from 59.69 euro cents.

* 51.97 British pence, from 52.08 British pence.

* 120.20 NZ cents, from 120.22 NZ cents.