Australia's share market has snapped a three week losing streak, but uncertainty hangs over investor sentiment as an oil supply route remains effectively blocked.

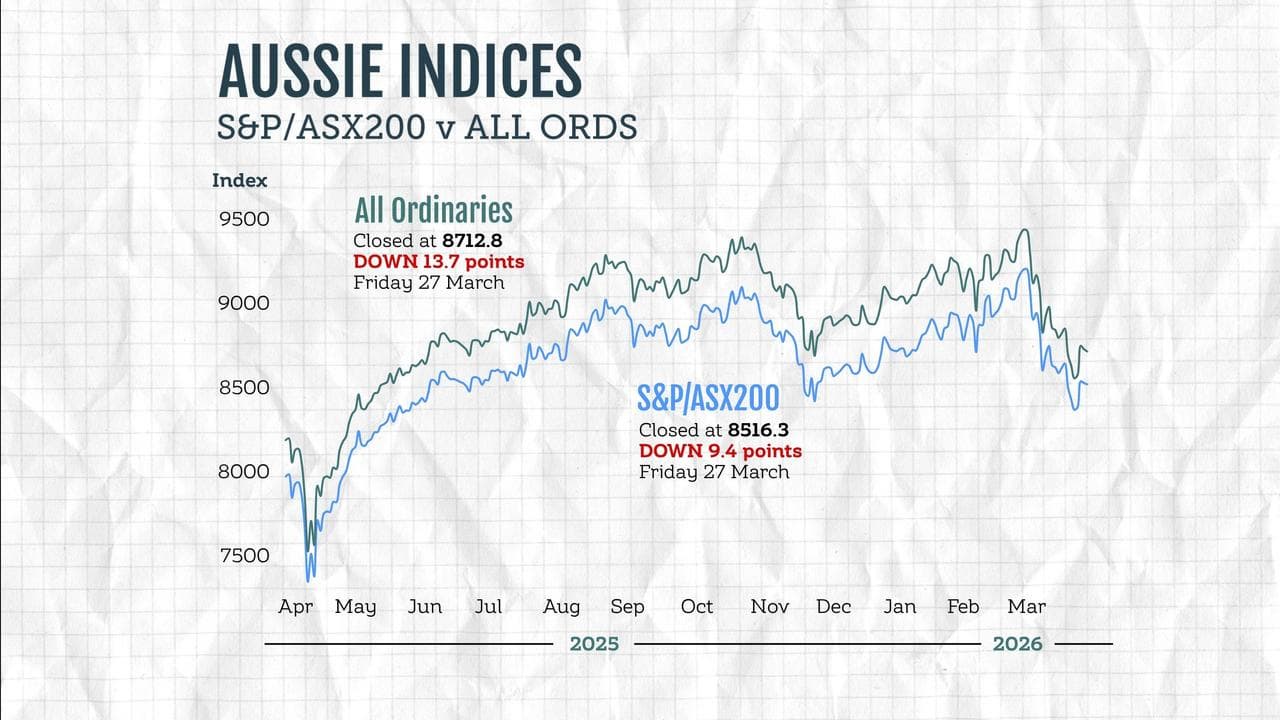

The S&P/ASX fell 9.4 points on Friday, down 0.11 per cent, to 8,516.3, as the broader All Ordinaries lost 13.7 points, or 0.16 per cent, to 8,712.8.

It was the first positive week for the bourse since US-led attacks on Iran sparked an energy price shock that has roiled global markets, but traders remain on edge with scarce common between the US and Iran to build a ceasefire upon.

More than $242 billion in value has been wiped from the local exchange's combined market capitalisation since the conflict began on February 28, although that figure was closer to $300 billion earlier this week.

"The key for global growth is to watch passageway through the Strait of Hormuz," AMP deputy chief economist Diana Mousina said.

"The longer this goes on, oil reserves will dwindle and shortages will become more of a problem and the oil price will spike higher."

Unsurprisingly local energy stocks outperformed the other 10 sectors, as Brent crude hovered above $US101, supporting local oil and gas giants Santos and Woodside.

Coal producers were also strong, with Whitehaven up almost fiver per cent after an upgrade from UBS, while uranium stocks faded from recent strength as risk sentiment dimmed.

Viva Energy and Ampol, which run Australia's two remaining oil refineries, each made ground on Friday and are up more than 38 per cent and 16 per cent respectively since the Iran conflict began.

Basic materials snatched their first positive week of the previous four, edging higher on Friday with help from mega miners BHP, Rio Tinto and Fortescue, as gold producers and most other sub sectors fell behind.

Gold is trading at $US4,442 ($A6,443) an ounce, hovering on par with its early January price and down roughly a quarter from all-time highs.

Lithium miners provided some relief, with Liontown and PLS each up more than 25 per cent for the week, as rising fuel prices fan interest in electric vehicles and electrification.

ASX-listed airlines were back in the red, with Qantas down 0.7 per cent and Virgin, which ordinarily runs direct flights to the Middle East, sinking 4.4 per cent.

The heavyweight financials sector has been just that, rounding out a fifth straight week of losses and down six per cent from mid-February's record peak.

Australia's consumer cyclicals sector snapped a nine-week losing run, the sector hanging on at a value on par with June 2024.

Consumer confidence was already under pressure before the Persian Gulf conflict lit a match under oil prices, sending inflation expectations soaring and pushing the Reserve Bank towards further interest rate hikes.

The combination of higher interest rates and inflation was likely to weigh on sentiment and economic growth, ANZ economists said.

"Real GDP growth is now expected to be 1.3 per cent year-on-year over 2026 and 1.8 per cent year-on-year in 2027, a material downward revision from our most recent forecasts," they wrote in a report.

The Australian dollar is buying 68.98 US cents, down from 69.47 US cents on Thursday at 5pm.

ON THE ASX:

* The S&P/ASX200 dropped 9.4 points, or 0.11 per cent, to 8,516.3

* The broader All Ordinaries fell 13.7 points, or 0.16 per cent, to 8,712.8

One Australian dollar trades for:

* 68.98 US cents, from 69.47 US cents at 5pm AEDT on Thursday

* 110.13 Japanese yen, from 110.81 Japanese yen

* 59.78 euro cents, from 60.12 euro cents

* 51.71 British pence, from 52.03 British pence

* 119.53 NZ cents, from 119.80 NZ cents