The Trump administration's efforts to topple the Iranian regime have liberated local investors from their money, wiping more than $120 billion from Australia's bourse in a week.

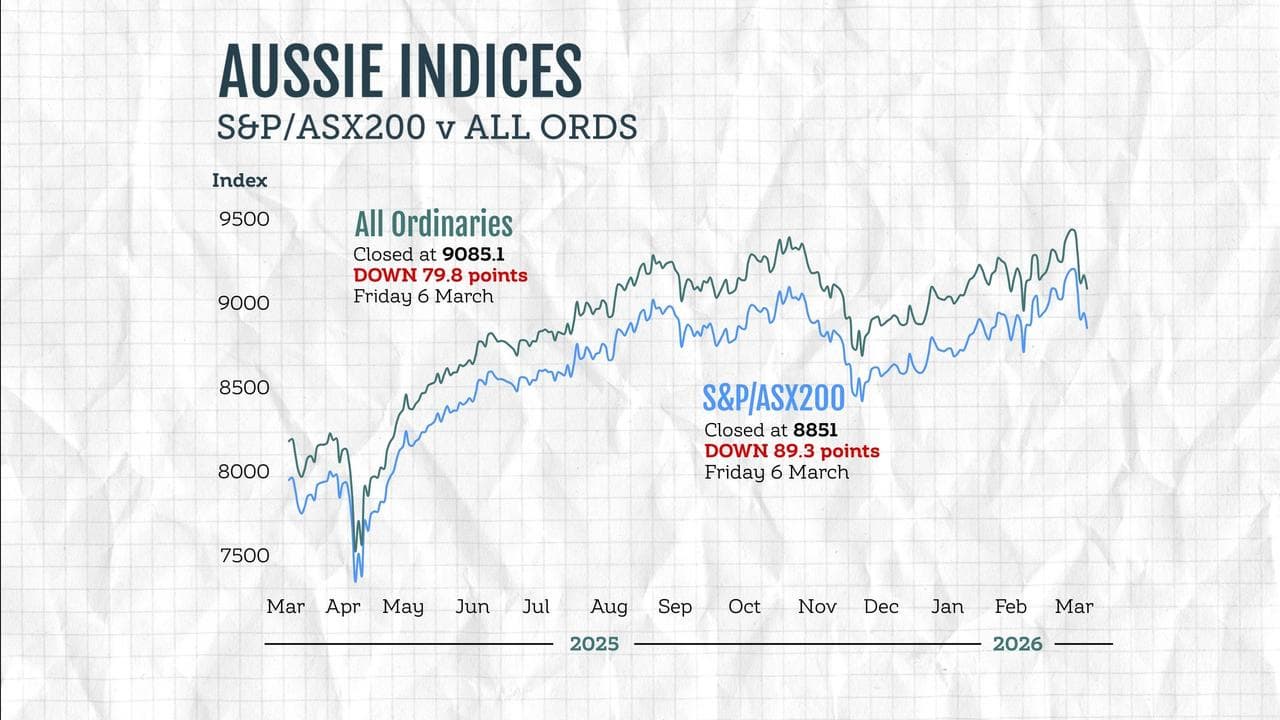

The S&P/ASX200 fell 89.3 points on Friday, down one per cent, to 8,851, as the broader All Ordinaries lost 79.8 points, or 0.87 per cent, to 9,085.1.

It was the top-200's worst weekly performance since early April 2025, when US president Donald Trump's Liberation Day tariff announcements roiled global markets.

The losses erased roughly $124 billion (3.9 per cent) from the top-500's $3.2 trillion combined market cap since the start of the week, as escalating conflict in the Middle East lit a match under oil prices, sparking fears of inflation and weaker global growth.

Local equities markets, and those in Asia and Europe had been rational in their response to the global events, according to Moomoo market strategist Michael McCarthy.

“It's not a disaster, it's not the end of the world,” he told AAP.

“At the same time, inflationary impulses are a very real risk, and the potential for an extended hit to global energy markets and the slowdown that would induce is also a real risk.

“Stagflation is something that we've been watching very carefully.”

More than 1000 people have been reported killed since the US and Israel bombed Iran last weekend, prompting retaliatory strikes on nearby US allies and broader regional conflict.

Local energy stocks soared more than seven per cent since Monday, less than half the appreciation of crude itself, supporting oil and gas giants Woodside and Santos.

The basic materials sector has been hammered this week, tumbling by a tenth and effectively wiping the previous 10 sessions of gains.

BHP shares have plunged even further to $52.81, selling off sharply after hitting multiple record highs the previous week, with a growth target downgrade from China on Thursday further dampening its outlook.

Iron ore futures have actually made gains, lifting $US101.90 ($A145.85) a tonne, but not enough to cover fears around growth, higher incoming input costs and ultimately lofty valuations.

Gold miners have been hammered, with local mining giant Northern Star down almost 15 per cent after initially spiking on safe haven buying on Monday, grinding lower as investors weighed a tighter interest rate outlook.

The precious metal is down 4.9 per cent since then to $US5,124 ($A7,282) an ounce, but remains historically high, worth double what it was at the beginning of 2025.

The heavyweight financials sector has had a grim week, tumbling more than three per cent as risk sentiment soured, although the Commonwealth Bank had some good news on Friday as Fitch upgraded the bank's credit rating to AA.

IT stocks have made a surprising recovery this week despite souring risk sentiment, as dip-buyers stepped into the beaten down sector.

The industrial segment has had a tough time, as flight disruptions weighed on Qantas and Virgin Australia via their Middle East partner airlines, made worse by higher projected jet fuel costs.

While there appeared to be no end in sight for the conflict, US mid-term elections later in 2026 could hold the key to a potential de-escalation, AMP economist My Bui said.

"Our base case is for Trump to find a way to declare victory before significant energy disruption and higher inflation expectations become entrenched," Ms Bui said.

"US voters’ number-one concern remains inflation and affordability, and with the midterm elections coming up, it is likely that Trump will take an off-ramp to limit consumer dissatisfaction."

The Australian dollar is buying 70.32 US cents, down from 70.41 US cents on Thursday at 5pm.

ON THE ASX:

* The S&P/ASX200 fell 89.3 points, or one per cent, to 8,851

* The broader All Ordinaries gained 79.8 points, or 0.87 per cent, to 9,085.1

CURRENCY SNAPSHOT:

One Australian dollar trades for:

* 70.32 US cents, from 70.41 US cents at 5pm AEDT on Thursday

* 110.98 Japanese yen, from 110.65 Japanese yen

* 60.58 euro cents, from 60.72 euro cents

* 52.64 British pence, from 52.88 British pence

* 119.11 NZ cents, from 119.00 NZ cents