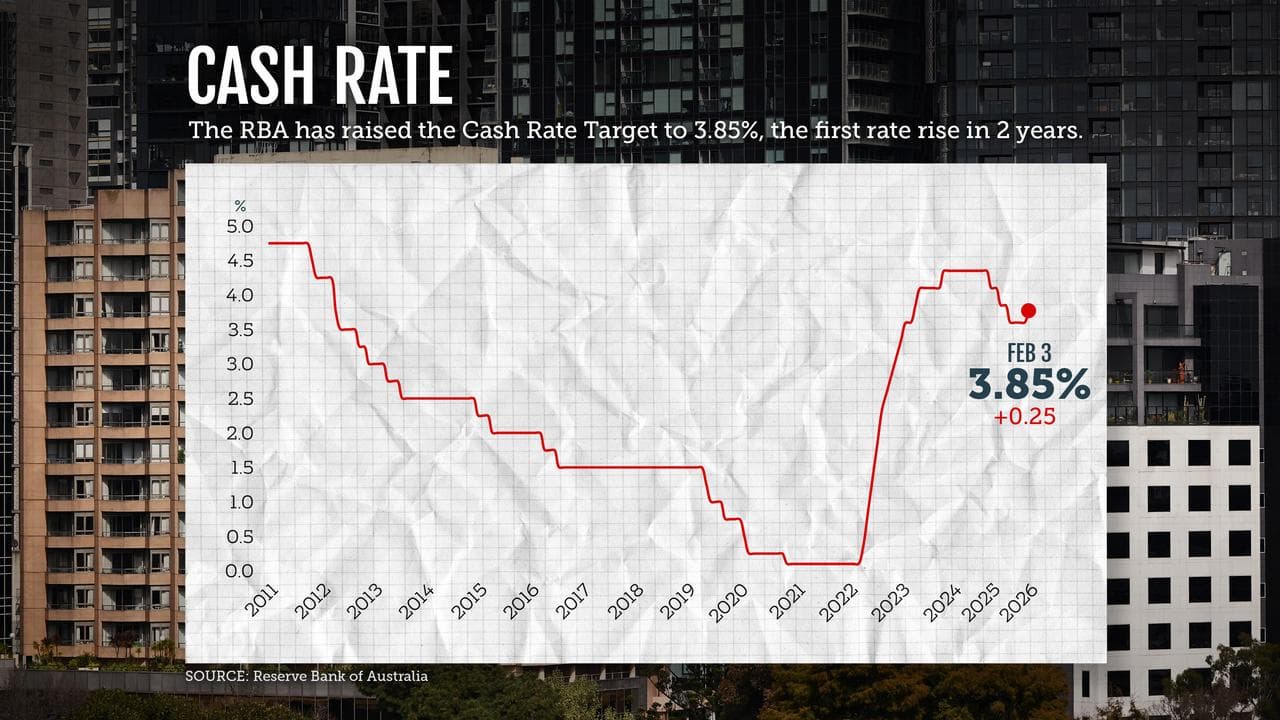

Traders upped their bets for a Reserve Bank rate hike in March to a one-in-three chance after the central bank's governor said the meeting would be "live".

While Michele Bullock was careful not to signpost the RBA's decision on March 17, her comments disabused any doves of the belief the board would only change the cash rate after quarterly inflation data, which is not due out until April.

Combined with stronger economic data also released on Tuesday, which prompted economists to increase GDP growth predictions, Ms Bullock's hawkish tone resulted in the odds of a rate hike jumping from 10 per cent to 33 per cent, IG market analyst Tony Sycamore said.

Speaking at the Australian Financial Review Business Summit in Sydney, Ms Bullock said the board would look at whether it needed to move even more quickly.

"I would discourage people from thinking that we necessarily only move every quarter," she said.

If expectations of stronger economic growth are borne out on Wednesday, that could heighten the RBA's fears the demand is outpacing supply and fuelling inflation.

NAB economists Jessie Cameron and Taylor Nugent revised up their GDP expectations for the December quarter from 0.6 per cent to one per cent after stronger public demand figures.

That would put annual GDP growth at 2.5 per cent - above the RBA's forecast of 2.3 per cent and its estimate of the highest economic growth rate that can be sustained without pushing up inflation.

Ms Bullock said the bank was closely watching events in the Middle East but it would take some time to make sense of their impact on domestic inflation.

"It’s too early to say what the impact will be. Events are moving rapidly and there are different ways this can play out," she told the summit on Tuesday.

"A supply shock could, for example, add to inflation pressures. And the potential implications for inflation expectations are something we are very alert to.

"But at the same time, a prolonged impact on energy markets could have adverse effects on global economic activity and result in downward pressure on inflation."

Crude prices on Tuesday were about 10 per cent higher than before the outbreak of conflict in Iran - one of the world's largest oil producers - which also threatened to shut supplies from other Middle Eastern nations from transiting through the Strait of Hormuz.

Given oil's role as an economy-wide input, a price surge threatens to have an outsized impact on global inflation, which is running well above the Reserve Bank's target.

In the worst-case scenario - in which the US becomes mired in a prolonged conflict with Iran and supplies are disrupted for longer - oil prices could double to about $US150 a barrel, AMP chief economist Shane Oliver said in a research note.

He ascribed a 40 per cent probability to such a scenario.

The Reserve Bank believed underlying demand was higher and the economy's supply potential was lower than what it assessed six months prior, Ms Bullock said, acknowledging its forecasts in 2025 were incorrect.

Jobs market indicators remained tight and it was uncertain whether financial conditions were restrictive enough to bring inflation back to target in a reasonable time, she said.